We have written in last quarter’s report that we should expect lower annual market returns than what were achieved in the previous 4 years. The reason for this has less to do with a change in the vigor, (or lack thereof) with which our economy grows and more to do with the price paid for assets in today’s environment. To explain let’s first review the rationale of any capital allocation decision and finish with discussing the significance of volatility and the need for unconventional thinking. The basis of any capital allocation decision has not changed since Aesop’s truism in 600 B.C., “a bird in the hand is worth two in the bush.” Warren Buffett, in his letter to shareholders in 2000, added three questions to this enduring axiom: 1) How certain are you that there are indeed birds in the bush? 2) When will they emerge and how many will there be? 3) What is the risk-free interest rate [how would your bird in hand grow without taking any risk]? Of course, in Buffett’s example birds are dollars and a bush is any capital outlay or investment. If you can answer these three questions with certainty, than you will know the maximum value of the bush (investment) and the maximum number of birds (dollars) that should be offered for it.

This theorem applies to stocks, bonds, March Madness brackets, lottery tickets, real estate, manufacturing plants, farms, or any capital outlay where income or gains are expected. There has not been any advancement in civilization since 600 B.C. that has changed this formula one iota. With the correct numbers in hand, one can rank the attractiveness of all possible capital outlays no matter the situation or location.

The question at hand is: Have the answers to the aforementioned questions changed at all?

If they have, then we should be happy trading more dollars to buy investments. If they haven’t, then we should resist the urge to pay more for investments. Of course it all depends on the investment. Regarding the US stock market, it is priced very near or above fair value and it is time to adjust our expectations. When looking at other sectors of the market, one can see substantial froth and overheating, especially in cloud, social networking and biotech. These areas provide a real risk to investor capital. As such, we should abandon our bias toward recent outsized returns and expect reduced returns going forward in those leading sectors.

With the outsized returns investors have recently experienced, we have also seen reduced volatility. This will not continue ad infinitum; instead let’s be prepared. For the prepared investor volatility brings opportunity.

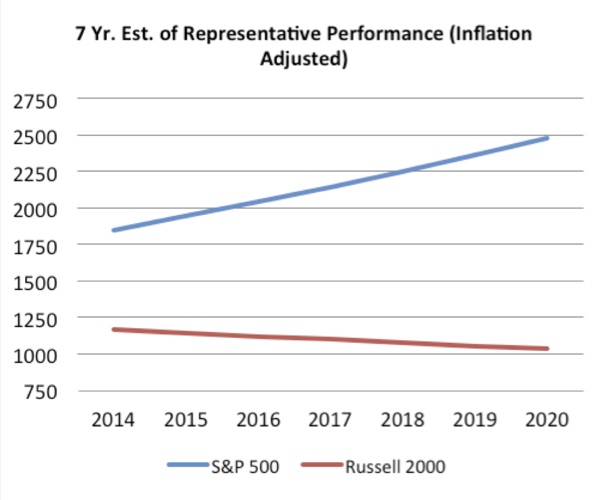

Let’s look at how this manifests itself: The following is a linear graph of our estimates of 7 year real returns. The graph shows our expectation of two major stock market indexes (S&P 500 representing large US companies and Russell 2000 representing small US companies).

The return lines are rather flat in both cases, especially the Russell 2000. Furthermore, they represent below average returns. Undoubtedly, volatility will come and go and these lines will not be flat at all. In fact stock price volatility will likely be more than we have recently experienced. According to QVM Group, 63% of quarters have nearly 10% downside volatility and 22% of quarters have nearly 20% downside volatility. On a side note, historical graphs rarely show this extreme volatility, instead showing average weekly prices that tend to level out some of the movement.

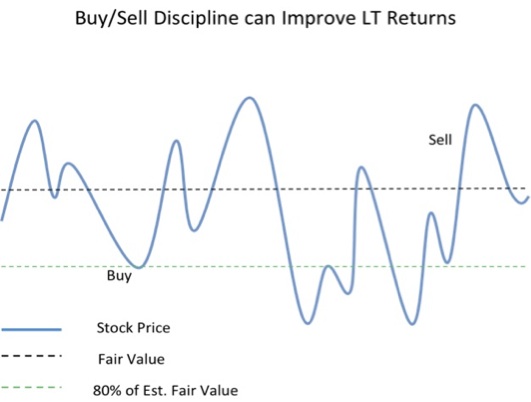

In the next graph, for illustration purposes we look at just the S&P 500 and insert random stock price volatility. We can reasonably expect opportunities to buy when it is undervalued. This requires vigilance in calculating fair value and thanks to Aesop (and Warren Buffett), we have a framework to determine it. It also requires discipline in only buying at a predetermined margin below fair value, in our example 80%. The safety that this margin creates is a key component of ensuring that if an assumption turns out to be incorrect, we may still achieve an acceptable return over the coming years.

Of course this is a very simple example and pressures to be invested and not “miss out” on returns can be extreme. Likewise, the fear inherent with buying when markets are down can be difficult to overcome. Most investors cannot subscribe to the unconventional wisdom required to assemble a portfolio that is different, which seeks to take advantage of normal volatility. These investors must be prepared to earn less in the coming years. There are simply not enough birds in the bush to justify current prices rising in line with historical averages.

An unconventional portfolio, with a slightly higher emphasis on liquidity and a tolerance for greater volatility will be necessary to earn higher returns. Investors in this market must weigh their requirement for earning greater than average market returns, versus the illusory safety and security of moving with the crowd. Normally, long-term perspective, patience and objectivity are crucial in managing an investment portfolio. Today, as much as anytime, we can emphasize the need to do things differently than what convention dictates.